Combo Backtest 123 Reversal & Finite Volume Elements (FVE) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The FVE is a pure volume indicator. Unlike most of the other indicators

(except OBV), price change doesn?t come into the equation for the FVE (price

is not multiplied by volume), but is only used to determine whether money is

flowing in or out of the stock. This is contrary to the current trend in the

design of modern money flow indicators. The author decided against a price-volume

indicator for the following reasons:

- A pure volume indicator has more power to contradict.

- The number of buyers or sellers (which is assessed by volume) will be the same,

regardless of the price fluctuation.

- Price-volume indicators tend to spike excessively at breakouts or breakdowns.

WARNING:

- For purpose educate only

- This script to change bars colors.

在腳本中搜尋"the strat"

Grid System With Fake MartingaleThe proposed strategy is based on a grid system with a money management that tries to replicate the effect of a martingale without having to double your position size after each loss, hence the name "fake martingale". Note that a balance using this strategy is still subject to exponential decay, the risk is not minimized, as such, it would be dangerous to use this strategy.

For more information on the martingale and grid systems see:

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the security you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, generating fewer trades as a result.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after each win.

How It Works

Let's illustrate how we replicate a martingale without doubling our exposure with a simple casino example. Imagine you are playing roulette, and that you are betting on colors (black/red), your payout is 1 to 1, in the case you win, you will have your initial stake back plus a profit equal to your initial stake.

If your strategy is to recover any previous losses, you can double your stake each time you lose, once you win you will get back the previous losses plus a profit equal to your original stake, this is the martingale system. So how can we win back previous losses without having to double our stake? We could do that by doubling the payout ratio after a loss, so after a loss, we must use a payout ratio of 2:1, if we lose once again we must use a payout of 4:1...etc, our payout ratio would be subject to exponential growth instead of our stake.

Of course, the payout ratio is fixed with casino games, but in trading, we can manipulate the position of our take profit in order to replicate such effect, this is what this strategy is doing. So after a loss, we place our take profit such that a win recover our losses back plus generate a profit.

Advantages

The advantage of this approach is that unlike the martingale we don't double our position size, which instead can remain constant, this is a huge advantage as a martingale will require a significant capital in order to tank a series of losses.

Disadvantages

The main disadvantage of this method is that the price might never reach our take profit after a long losing streak, our balance would remain in the red and we couldn't do anything about it except reset the strategy.

Frictional costs are still a disadvantage, as such, we would need to place our take profits in order to account for them, while this is still better than purchasing additional shares, it minimizes the chances of the price reaching the take profit.

Conclusions

An alternative money management system replicating the effect of a martingale as been presented, we can see that such a system is far from being perfect, and it would be foolish to use it, however, it stills offer a convenient alternative to less aggressive progressive position sizing systems.

I have been receiving some messages from users criticizing me for exposing the martingale money management system, and I understand why but I can't agree, talking about it allow me to warn users against it, the grid-martingale methodology is will create more harm than anything else, the reward is only one side of the story and should always be compared against the risk, so always take a look at all the statics in a backtest.

Thanks for reading!

Shout-Out

This post was made possible thanks to my patrons:

@Happymono, @AmariMars, @kkhaial, @Nugehe, @LucF, @Nosmok, @iflostio, @DankBeans, @ecletv, @Neverstorm, @alex.crown.jr, @uk503, @xkingshotss, @vsov, @jbelka, @yatrader2, @hughza, @ganh

Combo Backtest 123 Reversal & Extracting The Trend This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Extracting The Trend

The related article is copyrighted material from Stocks & Commodities Mar 2010

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Ergodic TSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

r - Length of first EMA smoothing of 1 day momentum 4

s - Length of second EMA smoothing of 1 day smoothing 8

u- Length of third EMA smoothing of 1 day momentum 6

Length of EMA signal line 3

Source of Ergotic TSI Close

This is one of the techniques described by William Blau in his book "Momentum,

Direction and Divergence" (1995). If you like to learn more, we advise you to

read this book. His book focuses on three key aspects of trading: momentum,

direction and divergence. Blau, who was an electrical engineer before becoming

a trader, thoroughly examines the relationship between price and momentum in

step-by-step examples. From this grounding, he then looks at the deficiencies

in other oscillators and introduces some innovative techniques, including a

fresh twist on Stochastics. On directional issues, he analyzes the intricacies

of ADX and offers a unique approach to help define trending and non-trending periods.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Ergodic MDI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is one of the techniques described by William Blau in his book "Momentum,

Direction and Divergence" (1995). If you like to learn more, we advise you to

read this book. His book focuses on three key aspects of trading: momentum,

direction and divergence. Blau, who was an electrical engineer before becoming

a trader, thoroughly examines the relationship between price and momentum in

step-by-step examples. From this grounding, he then looks at the deficiencies

in other oscillators and introduces some innovative techniques, including a

fresh twist on Stochastics. On directional issues, he analyzes the intricacies

of ADX and offers a unique approach to help define trending and non-trending periods.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Ergodic MACD This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is one of the techniques described by William Blau in his book

"Momentum, Direction and Divergence" (1995). If you like to learn more,

we advise you to read this book. His book focuses on three key aspects

of trading: momentum, direction and divergence. Blau, who was an electrical

engineer before becoming a trader, thoroughly examines the relationship

between price and momentum in step-by-step examples. From this grounding,

he then looks at the deficiencies in other oscillators and introduces some

innovative techniques, including a fresh twist on Stochastics. On directional

issues, he analyzes the intricacies of ADX and offers a unique approach to help

define trending and non-trending periods.

Blau`s indicator is like usual MACD, but it plots opposite of meaningof

stndard MACD indicator.

WARNING:

- For purpose educate only

- This script to change bars colors.

Grid Like StrategyIt is possible to use progressive position sizing in order to recover from past losses, a well-known position sizing system being the "martingale", which consists of doubling your position size after a loss, this allows you to recover any previous losses in a losing streak + winning an extra. This system has seen a lot of attention from the trading community (mostly from beginners), and many strategies have been designed around the martingale, one of them being "grid trading strategies".

While such strategies often shows promising results on paper, they are often subjects to many frictions during live trading that makes them totally unusable and dangerous to the trader. The motivations behind posting such a strategy isn't to glorify such systems, but rather to present the problems behind them, many users come to me with their ideas and glorious ways to make money, sometimes they present strategies using the martingale, and it is important to present the flaws of this methodology rather than blindly saying "you shouldn't use it".

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the symbol you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, as such higher values will generate fewer trades.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after any wins.

The Grid

Grid strategies are commons and do not present huge problems until we use certain position sizing methods such as the martingale. A martingale is extremely sensitive to any kind of friction (frictional costs, slippage...etc), the grid strategy aims to provide a stable and simple environment where a martingale might possibly behave well.

The goal of a simple grid strategy is to go long once the price crossover a certain level, a take profit is set at the level above the current one and stop loss is placed at the level below the current one, in a winning scenario the price reach the take profit, the position is closed and a new one is opened with the same setup. In a losing scenario, the price reaches the stop loss level, the position is closed and a short one is opened, the take profit is set at the level below the current one, and a stop loss is set at the level above the current one. Note that all levels are equally spaced.

It follows from this strategy that wins and losses should be constant over time, as such our balance would evolve in a linear fashion. This is a great setup for a martingale, as we are theoretically assured to recover all the looses in a losing streak.

Martingale - Exponential Decays - Risk/Reward

By using a martingale we double our position size (exposure) each time we lose a trade, if we look at our balance when using a martingale we see significant drawdowns, with our balance peaking down significantly. The martingale sequence is subject to exponential growth, as such using a martingale makes our balance exposed to exponential decays, that's really bad, we could basically lose all the initially invested capital in a short amount of time, it follows from this that the theoretical success of a martingale is determined by what is the maximum losing streak you can endure

Now consider how a martingale affects our risk-reward ratio, assuming unity position sizing our martingale sequence can be described by 2^(x-1) , using this formula we would get the amount of shares/contracts we need to purchase at the x trade of a losing streak, we would need to purchase 256 contracts in order to recover from a losing streak of size 9, this is enormous when you take into account that your wins are way smaller, the risk-reward ratio is totally unfair.

Of course, some users might think that a losing streak of size 9 is pretty unlikely, if the probability of winning and losing are both equal to 0.5, then the probability of 9 consecutive losses is equal to 0.5^9 , there are approximately 0.2% of chance of having such large losing streak, note however that under a ranging market such case scenario could happen, but we will see later that the length of a losing streak is not the only problem.

Other Problems

Having a capital large enough to tank 9any number of consecutive losses is not the only thing one should focus on, as we have to take into account market prices and trading dynamics, that's where the ugly part start.

Our first problem is frictional costs, one example being the spread, but this is a common problem for any strategy, however here a martingale is extra sensitive to it, if the strategy does not account for it then we will still double our positions costs but we might not recover all the losses of a losing streak, instead we would be recovering only a proportion of it, under such scenario you would be certain to lose over time.

Another problem are gaps, market price might open under a stop-loss without triggering it, and this is a big no-no.

Equity of the strategy on AMD, in a desired scenario the equity at the second arrow should have been at a higher position than the equity at the first arrow.

In order for the strategy to be more effective, we would need to trade a market that does not close, such as the cryptocurrency market. Finally, we might be affected by slippage, altho only extreme values might drastically affect our balance.

The Anti Martingale

The strategy lets you use an anti-martingale, which double the position size after a win instead of a loss, the goal here is not to recover from a losing strike but instead to profit from a potential winning streak.

Here we are exposing your balance to exponential gross but you might also lose a trade at the end a winning streak, you will generally want to reinitialize your position size after a few wins instead of waiting for the end of a streak.

Alternative

You can use other-kind of progressions for position sizing, such as a linear one, increasing your position size by a constant number each time you lose. More gentle progressions will recover a proportion of your losses in a losing streak.

You can also simulate the effect of a martingale without doubling your position size by doubling your target profit, if for example you have a 10$ profit-target/stop-loss and lose a trade, you can use a 20$ profit target to recover from the lost trade + gain a profit of 10$. While this approach does not introduce exponential decay in your balance, you are betting on the market reaching your take profits, considering the fact that you are doubling their size you are expecting market volatility to increase drastically over time, as such this approach would not be extremely effective for high losing streak.

Conclusion

You will see a lot of auto-trading strategies that are based on a grid approach, they might even use a martingale. While the backtests will look appealing, you should think twice before using such kind of strategy, remember that frictional costs will be a huge challenge for the strategy, and that it assumes that the trader has an important initial capital. We have also seen that the risk/reward ratio is theoretically the worst you can have on a strategy, having a low reward and a high risk. This does not mean that progressive position sizing is bad, but it should not be pushed to the extreme.

It is nice to note that the martingale is originally a betting system designed for casino games, which unlike trading are not subject to frictional costs, but even casino players don't use it, so why would you?

Thx for reading

Combo Backtest 123 Reversal & Ergodic CSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is one of the techniques described by William Blau in his book

"Momentum, Direction and Divergence" (1995). If you like to learn more,

we advise you to read this book. His book focuses on three key aspects

of trading: momentum, direction and divergence. Blau, who was an electrical

engineer before becoming a trader, thoroughly examines the relationship between

price and momentum in step-by-step examples. From this grounding, he then looks

at the deficiencies in other oscillators and introduces some innovative techniques,

including a fresh twist on Stochastics. On directional issues, he analyzes the

intricacies of ADX and offers a unique approach to help define trending and

non-trending periods.

This indicator plots Ergotic CSI and smoothed Ergotic CSI to filter out noise.

WARNING:

- For purpose educate only

- This script to change bars colors.

Custom Screener with Alerts [QuantNomad]Some time ago I published an example of simple custom screener in PineScript:

The only thing this screener did is created a dynamic label with screener output.

Recently TradingView announced alerts from the strategy with the possibility to add custom messages to alerts.

So using it I was able to create a bit more advanced screener which sends results as alert messages. With tools like Alertatron, you can easily redirect them to Telegram if you want.

It works for 40 symbols (limitation of the number of security calls).

To create your own screener you need to change only screenerFunc. The logic of this function is very simple, it outputs value you want to display in screener and condition based on which your screener should filter your stocks.

To create alerts for this screener create an alert from strategy and use {{strategy.order.alert_message}} as alert message.

Do you know now how to make this screener better? Let me know.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

Combo Backtest 123 Reversal & Empirical Mode Decomposition This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from Stocks & Commodities Mar 2010

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Elder Ray (Bull Power) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Developed by Dr Alexander Elder, the Elder-ray indicator measures buying

and selling pressure in the market. The Elder-ray is often used as part

of the Triple Screen trading system but may also be used on its own.

Dr Elder uses a 13-day exponential moving average (EMA) to indicate the

market consensus of value. Bull Power measures the ability of buyers to

drive prices above the consensus of value. Bear Power reflects the ability

of sellers to drive prices below the average consensus of value.

Bull Power is calculated by subtracting the 13-day EMA from the day's High.

Bear power subtracts the 13-day EMA from the day's Low.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Elder Ray (Bear Power) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Developed by Dr Alexander Elder, the Elder-ray indicator measures buying

and selling pressure in the market. The Elder-ray is often used as part

of the Triple Screen trading system but may also be used on its own.

Dr Elder uses a 13-day exponential moving average (EMA) to indicate the

market consensus of value. Bull Power measures the ability of buyers to

drive prices above the consensus of value. Bear Power reflects the ability

of sellers to drive prices below the average consensus of value.

Bull Power is calculated by subtracting the 13-day EMA from the day's High.

Bear power subtracts the 13-day EMA from the day's Low.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

KD compare strategy (交易策略對照組)This is a base and easy trading strategy for comparing my other strategy.

The strategy consider K >= 80 is strong target in the last high period,

and consider K <=20 is the weak target in the last low period.

In the strong target, the strategy may increase long at the first day when K < 50, until 2/3 max order limitation or strong target become to weak.

In the weak target, the strategy may increase short at the first day when K > 50, until 2/3 max order limitation or strong target become to strong.

there are three orders for this strategy.

when the strong become to weak, it may use the remain 1/3 to save itself, and change the direction at the next k > 50

when the weak become to weak, it may use the remain 1/3 to save itself, and change the direction at the next k < 50

這是一個簡單的雙向交易策略,用來對照我其他的策略。

當 K>=80 它會認為目前是強勢股,偏多操作

當 K<=20 它會認為目前是強勢股,偏空操作

當標的為強勢股時,當第一次 K<50 會加碼多單,最多買進2/3的持股,直到轉弱

當標的為弱勢股時,當第一次 K>50 會加碼空單,最多買進2/3的持股,直到轉強

當強勢轉弱勢時,會使用剩下的1/3來拯救持股,在下次 k > 50 出清持股

當弱勢轉強勢時,會使用剩下的1/3來拯救持股,在下次 k < 50 出清持股

Combo Backtest 123 Reversal & Elder Ray (Bear Power) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Developed by Dr Alexander Elder, the Elder-ray indicator measures buying

and selling pressure in the market. The Elder-ray is often used as part

of the Triple Screen trading system but may also be used on its own.

Dr Elder uses a 13-day exponential moving average (EMA) to indicate the

market consensus of value. Bear Power measures the ability of sellers to

drive prices below the consensus of value. Bear Power reflects the ability

of sellers to drive prices below the average consensus of value.

Bull Power is calculated by subtracting the 13-day EMA from the day's High.

Bear power subtracts the 13-day EMA from the day's Low.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

eha Moving Averages StrategyMoving Average based strategies are very popular ones among both long-term investors and short-term traders as they can be tailored to any time frame. One of the main moving average strategies are crossovers. The very simple type is a price crossover , which is when the price crosses above or below a moving average to signal a potential change in trend.

Another strategy is to apply two moving averages to a chart: one longer (or slow) and one shorter (or fast). When the shorter-term MA crosses above the longer-term MA, it's a buy signal, as it indicates that the trend is shifting up (also known as “ Golden Cross ”). Meanwhile, when the shorter-term MA crosses below the longer-term MA, it's a sell signal, as it indicates that the trend is shifting down (which is also known as “ Dead/Death Cross ”).

This is a study to find a suitable trading strategy for 4-6 hour time frames. As you can see the performance is currently very poor. It has just generated almost 90 trades in a very long period from January 2017 to the time of publishing the study for the first time.

Moving averages work quite well in strong trending conditions but poorly in choppy or ranging conditions. Adjusting the time frame can correct this problem temporarily, although, at some point, these issues are likely to occur regardless of the time frame chosen for the moving average(s).

I am working on this basic strategy to make its performance better and I will update the post in the future. So keep in touch by following the post.

Why have I republished my study?

It sounds like TradingView stores and indexes scripts based on the title of the post rather than the actual title of the scripts and if one chose general terms as the title of the post, the TradingView script search engine may be unable to find it. So I decided to repost the strategy with a more searchable and unique prefix of " eha ".

Please provide me with your precious feedback.

MTF Trailing SL Alerts [QuantNomad]These are alerts for my MTF Trailing SL Strategy.

Entry Long position if all 4 time-frames agree on the long signal.

Exit Long positions when at least 2 time-frames disagree on the long signals.

Entry to Short position if all 4 time-frames agree on Short signal.

Exit from Short positions when at least 2 time-frames disagree on Short signal.

Use "Once Per Bar Close" when creating alerts.

Link to the strategy:

Combo Backtest 123 Reversal & Ease of Movement (EOM) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator gauges the magnitude of price and volume movement.

The indicator returns both positive and negative values where a

positive value means the market has moved up from yesterday's value

and a negative value means the market has moved down. A large positive

or large negative value indicates a large move in price and/or lighter

volume. A small positive or small negative value indicates a small move

in price and/or heavier volume.

A positive or negative numeric value. A positive value means the market

has moved up from yesterday's value, whereas, a negative value means the

market has moved down.

WARNING:

- For purpose educate only

- This script to change bars colors.

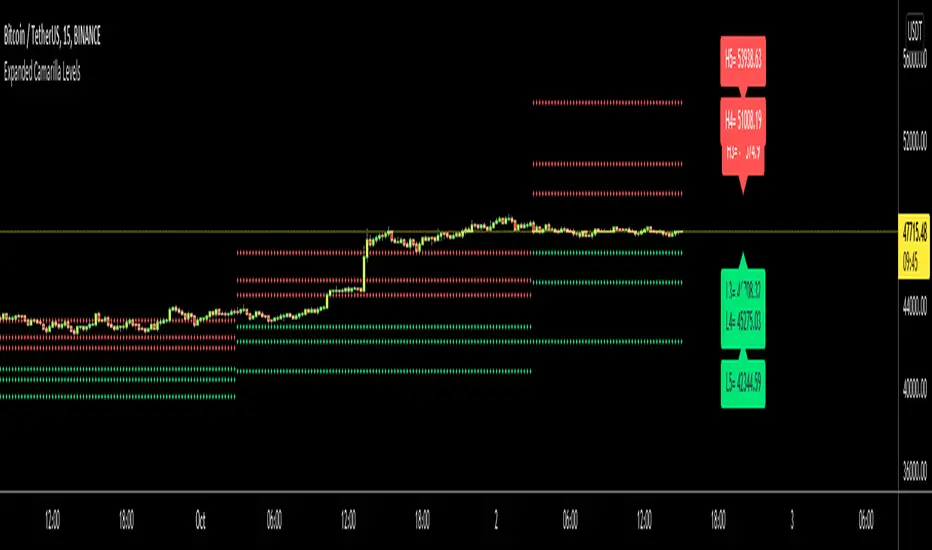

Expanded Camarilla LevelsHello Everyone,

The Expanded Camarilla Level s is introduced in the book " Secrets of a Pivot Boss: Revealing Proven Methods for Profiting in the Market " by Franklin Ocho a. I will not write a lot about the book, you should read it for yourself. There are many great ideas in the book, such using these levels, following trend, time price opportunity, Advanced Camarilla Concepts and much more.

The definition/formula of the levels defined in the book. ( actualy L1, L2, H1 and H2 levels are not used in the strategy, so not shown on the chart )

RANGE = highhtf - lowhtf

H5 = (HIGH/ LOW) * CLOSE

H4 = CLOSE + RANGE * 1.1/2

H3 = CLOSE+ RANGE * 1.1/4

H2 = CLOSE+ RANGE * 1.1/6

H1 = CLOSE+ RANGE * 1.1/12

L1 = CLOSE- RANGE * 1.1/12

L2 = CLOSE- RANGE * 1.1/6

L3 = CLOSE- RANGE * 1.1/4

L4 = CLOSE- RANGE * 1.1/2

L5 = CLOSE- (H5 - CLOSE)

Levels:

Strategy: you need to take care of the candles, as you can see there is bearish candle on first part, and Bullish Candle on second part!

Another Strategy:

An Example:

ENJOY!

Combo Backtest 123 Reversal & Dynamo This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

In July 1996 Futures magazine, E. Marshall Wall introduces the

Dynamic Momentum Oscillator (Dynamo). Please refer to this article

for interpretation.

The Dynamo oscillator is a normalizing function which adjusts the

values of a standard oscillator for trendiness by taking the difference

between the value of the oscillator and a moving average of the oscillator

and then subtracting that value from the oscillator midpoint.

WARNING:

- For purpose educate only

- This script to change bars colors.

Underworld Hunter Backtesting AlgorhitmThis strategy is built to prove the profitability of my Underworld Hunter indicator . It tests two different strategies. I won't be going into the calculation again since it is part of the original script. I just made a few adjustments.

First one is clearly visual. It plots slimmer twin-coloured lines now and has a different colour for every extreme level. Second is less obvious - I switched Relative Strength Index for Commodity Channel Index.

Extreme levels are as follows: green 100 -► 120, yellow 120 -► 140, orange 140 -► 160, red 160 -► 180 and purple above 180, I will have a special separate algorithm for testing optimal CCI levels someday, in this script, these values are only meant to help you with manual operations and do not influence results of the strategy in any way.

#Trending strategy

The trending strategy opens a position whenever the price leaves the bands and holds it until two consecutive bars are closed within the bands. The picture shows one winning position that hasn't yet been resulted. It also shows a few fakeouts. For this strategy, you want to keep the length below 110, the deviation should be below 2 and you probably want to play lower timeframes.

#Within the bands

The second strategy is pretty much the opposite. It opens a position when the price reaches outer bands and holds it until two consecutive bars are closed within the bands and current bar closes below previous bars low in case of long. It is working on hourly timeframes and you need higher length and deviation to succeed. The picture shows a few positions on EURUSD. Each of them is profitable but would be much higher if you closed it manually when it was time. You need to enable this strategy, which automatically disables the other one.

When using my script, you need to bear in mind that the first strategy doesn't detect optimal levels to close the price. A trend is often followed by a less volatile and boring correction which causes bands to shrink and lower your profits if you don't close manually as it will take longer till bands are reached.

On the other hand, second script literally has no stop-loss. As long as the price is outside the range, it will never close which will cause major drawdowns, unless you control the trade manually. CCI is here to help you with both.

I also recommend combining this with Market Profile (on TW, there is only Volume Profile, which can be used in a similar way) and trading day theory (trending with multiple distributions, trending day, normal day, a variation on a normal day, non-trending day or neutral day). Always keep in mind that it is up to traders to be profitable, indicators can support a good trader, but they will not fix a bad one.

Price Action and 3 EMAs Momentum plus Sessions FilterThis indicator plots on the chart the parameters and signals of the Price Action and 3 EMAs Momentum plus Sessions Filter Algorithmic Strategy. The strategy trades based on time-series (absolute) and relative momentum of price close, highs, lows and 3 EMAs.

I am still learning PS and therefore I have only been able to write the indicator up to the Signal generation. I plan to expand the indicator to Entry Signals as well as the full Strategy.

The strategy works best on EURUSD in the 15 minutes TF during London and New York sessions with 1 to 1 TP and SL of 30 pips with lots resulting in 3% risk of the account per trade. I have already written the full strategy in another language and platform and back tested it for ten years and it was profitable for 7 of the 10 years with average profit of 15% p.a which can be easily increased by increasing risk per trade. I have been trading it live in that platform for over two years and it is profitable.

Contributions from experienced PS coders in completing the Indicator as well as writing the Strategy and back testing it on Trading View will be appreciated.

STRATEGY AND INDICATOR PARAMETERS

Three periods of 12, 48 and 96 in the 15 min TF which are equivalent to 3, 12 and 24 hours i.e (15 min * period / 60 min) are the foundational inputs for all the parameters of the PA & 3 EMAs Momentum + SF Algo Strategy and its Indicator.

3 EMAs momentum parameters and conditions

• FastEMA = ema of 12 periods

• MedEMA = ema of 48 periods

• SlowEMA = ema of 96 periods

• All the EMAs analyse price close for up to 96 (15 min periods) equivalent to 24 hours

• There’s Upward EMA momentum if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA

• There’s Downward EMA momentum if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA

PA momentum parameters and conditions

• HH = Highest High of 48 periods from 1st closed bar before current bar

• LL = Lowest Low of 48 periods from 1st closed bar from current bar

• Previous HH = Highest High of 84 periods from 12th closed bar before current bar

• Previous LL = Lowest Low of 84 periods from 12th closed bar before current bar

• All the HH & LL and prevHH & prevLL are within the 96 periods from the 1st closed bar before current bar and therefore indicative of momentum during the past 24 hours

• There’s Upward PA momentum if price close > HH and HH > prevHH and LL > prevLL

• There’s Downward PA momentum if price close < LL and LL < prevLL and HH < prevHH

Signal conditions and Status (BuySignal, SellSignal or Neutral)

• The strategy generates Buy or Sell Signals if both 3 EMAs and PA momentum conditions are met for each direction and these occur during the London and New York sessions

• BuySignal if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA and price close > HH and HH > prevHH and LL > prevLL and timeinrange (LDN&NY) else Neutral

• SellSignal if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA and price close < LL and LL < prevLL and HH < prevHH and timeinrange (LDN&NY) else Neutral

Entry conditions and Status (EnterBuy, EnterSell or Neutral)(NOT CODED YET)

• ENTRY IS NOT AT THE SIGNAL BAR but at the current bar tick price retracement to FastEMA after the signal

• EnterBuy if current bar tick price <= FastEMA and current bar tick price > prevHH at the time of the Buy Signal

• EnterSell if current bar tick price >= FastEMA and current bar tick price > prevLL at the time of the Sell Signal

Combo Backtest 123 Reversal & Dynamic Pivot Point This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This Pivot points is calculated on the current day.

Pivot points simply took the high, low, and closing price from the previous period and

divided by 3 to find the pivot. From this pivot, traders would then base their

calculations for three support, and three resistance levels. The calculation for the most

basic flavor of pivot points, known as ‘floor-trader pivots’, along with their support and

resistance levels.

WARNING:

- For purpose educate only

- This script to change bars colors.

My VWAP Reversal + Pivot Points StandardThis indicator, with the addition of a standard VWAP indicator to the 5m chart, helps the operator when using a closing candle Price to initiate a VWAP Reversal strategy.

The strategy involves Price gapping up, look for a Close below the 1st 5m candle Low; else look for a Close above the 1st 5m candle High. On a break of VWAP, take the trade in the opposite direction of the gap, hence the VWAP Reversal. Not my own strat, credit to T3 Newsbeat, publicly posted on YouTube.

The Pivot Points Standard in the Pine 4 user manual, was the base source code, and leaving it here will allow me to remove the PP indicator I was using.